If your inbox has been flooded with confusing notifications from your student loan servicer lately, take a deep breath. You are definitely not alone.

Between fierce federal court battles dismantling older programs and the sweeping rollout of the One Big Beautiful Bill Act (OB3), the world of federal student loan payment plans has just gone through its biggest transformation in a generation.

Starting July 1, 2026, the old system is officially being mothballed for new borrowers. The confusing alphabet soup of choices you used to face like PAYE, ICR, and the highly debated SAVE plan is gone. Moving forward, the government is consolidating the federal repayment framework into just two core pathways.

Whether you are a fresh college graduate staring down your very first bill, an existing borrower trying to figure out if you’re grandfathered in, or a parent navigating funding for your kids, this absolute guide will break down the new student loan payment plans without the annoying legal jargon.

The Chaos Before the Calm: Why Everything Changed in 2026

To understand where your monthly money is going, we have to look briefly at how we got here. For the last few years, federal repayment was in a state of constant legal limbo. The Biden administration’s SAVE plan, which offered lower payments and faster paths to forgiveness, was tied up in courts for months before a federal appeals court ordered its final dismantlement.

Hot on the heels of those legal rulings came the implementation of the One Big Beautiful Bill Act. Signed into law to dramatically simplify federal financial aid, this act wipes the slate clean.

Instead of forcing you to decipher half a dozen overlapping income-driven tracks, the new policy mandates that all new federal borrowers choose between two distinct student loan payment plans: an income-sensitive track and a modified fixed track.

Let’s look at exactly how these two options function.

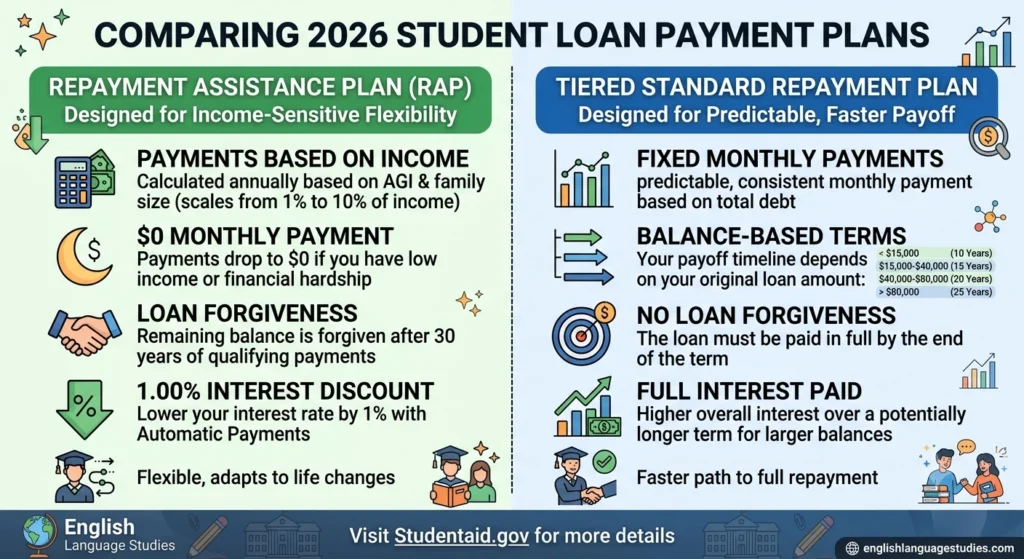

Option 1: The Repayment Assistance Plan (RAP)

If you need a safety net that shifts based on your economic reality, the Repayment Assistance Plan (RAP) is your new default income-driven option.

RAP behaves similarly to older income-driven frameworks but features a completely overhauled formula. Your required monthly amount is calculated entirely using a straightforward assessment of what you earn relative to your household size and number of dependents. If you experience an unexpected job loss or a drop in salary, your required payment can drop all the way to $0 automatically.

The Major Incentive: An Interest Rate Discount

In a surprising move to incentivize voluntary enrollment and consistent tracking, the Department of Education has attached a notable perk to RAP: if you sign up for auto-pay under this plan, the government will knock a full 1.00 percentage point off your loan’s interest rate. Given that average federal interest rates have hovered at uncomfortable highs recently, dropping an 8% rate down to 7% can save you thousands of dollars over the lifetime of your debt.

The Catch: A Much Longer Road to Forgiveness

While the lower monthly payments and interest rate discounts sound like an absolute win, the law balances the scales by extending the timeline required for total debt cancellation. Under legacy income-driven frameworks, remaining balances were typically forgiven after 20 or 25 years of steady payments. Under the new RAP rules, forgiveness takes a full 30 years, regardless of whether your debt was for undergraduate or graduate studies.

Option 2: The Tiered Standard Repayment Plan

Not everyone wants to share their tax returns with the federal government every year, and not everyone wants their debt hanging over their heads for three decades. If you prefer a highly predictable, set-it-and-forget-it monthly bill, you will land in the newly minted Tiered Standard Repayment Plan.

Historically, the standard option was a rigid 10-year timeline. If you graduated with $80,000 in debt, your monthly bill was astronomically high because you were forced to compress that principal into 120 even payments. The new Tiered Standard framework changes this entirely by scaling your payoff window based directly on how much total money you originally borrowed.

This tiered system ensures that individuals with massive balances aren’t crushed by immediate, unmanageable monthly premiums right out of school. However, a longer term means you will be paying interest across a much wider window of time.

Live 2026 Student Loan Calculator

To see exactly how these changes apply to your specific financial situation, use our interactive simulator below. Adjust your total balance, income, and household size to see your estimated monthly commitments under both tracks side-by-side.

2026 Student Loan Payment Estimator

Compare the new RAP vs. Tiered Standard plans under the 2026 OB3 Act rules.

Repayment Assistance Plan (RAP)

Tiered Standard Plan

Comparing the New 2026 Options At-a-Glance

To help you see how these structural changes match up against one another over the long haul, let’s look at how the Tiered Standard timelines scale alongside the flexible rules of the RAP.

| Repayment Feature | The Repayment Assistance Plan (RAP) | The Tiered Standard Plan |

| Monthly Payment Basis | Discretionary income & family size | Total outstanding loan balance |

| Payment Stability | Fluctuates annually based on tax data | Fixed monthly amount |

| Available Terms | Up to 30 years | 10, 15, 20, or 25 years (based on balance) |

| Interest Benefits | 1% rate reduction via auto-pay | Standard statutory interest rates |

| Forgiveness Eligibility | Remaining balance forgiven after 30 years | No forgiveness (loan is paid to $0) |

The Grandfather Window: What Happens to Current Borrowers?

If you are already out of school and currently utilizing an older repayment track, do not panic just yet. The new legislation does not immediately pull the rug out from under you, but it does set a definitive countdown clock.

Existing borrowers have a transition window that runs until July 1, 2028, to migrate their accounts over to the new 2026 framework. If you are sitting comfortably on a legacy plan that fits your budget perfectly, you can generally stay put for the next two years.

Critical Warning: The moment you take out any new federal loans—for instance, if you decide to go back to school for a graduate degree or professional certification—the grandfather protection shatters. Any new disbursement will permanently shift your entire federal portfolio into the new system, leaving you with only the RAP or the Tiered Standard tracks as choices.

Furthermore, if you were one of the 7 million Americans caught in limbo by the sudden termination of the SAVE plan, your administrative forbearance is winding down. You will need to proactively log into your loan servicer’s portal to select an alternative pathway before standard billing cycles resume in full force.

A Quick Word on the New Caps for Parents and Graduate Students

The changes implemented this year don’t just transform your choices among student loan payment plans; they also fundamentally change how much debt future students can accumulate.

If you are planning to utilize Grad PLUS or Parent PLUS loans, the One Big Beautiful Bill Act has introduced strict statutory limits to curb skyrocketing debt:

- Graduate & Professional Programs: Strict caps are now set at $20,500 per year for standard graduate programs, with a combined lifetime borrowing limit of $257,500.

- Parent PLUS Loans: These are now capped strictly at $20,000 per student, per year, with a lifetime maximum of $65,500 per dependent child.

These borrowing restrictions mean that finding an affordable, predictable repayment path is more critical than ever, as families will have to rely more on calculated budgeting and less on unlimited federal borrowing.

Strategic Playbook: Which Plan Should You Actually Choose?

When it comes down to making a final decision, look past the political noise and focus entirely on your personal cash flow and debt-to-income ratio.

Lean Toward the Repayment Assistance Plan (RAP) If:

Your total loan balance is significantly higher than your projected annual entry-level salary. For example, if you owe $70,000 but are starting out in a field making $45,000, the Tiered Standard plan will demand a rigid percentage of your income that might compromise your ability to pay rent.

RAP protects you against lean years, gives you breathing room if you have children, and drops your structural interest rate by a full point via auto-pay. Just keep in mind that you are signing up for a very long-term relationship with your loan servicer.

Lean Toward the Tiered Standard Plan If:

You possess a highly stable, predictable income that easily covers your foundational living expenses with money left over. If your primary goal is to minimize the total amount of money you throw away on compounding interest, the Tiered Standard plan is your best bet. By locking in a fixed timeline, you ensure that every single monthly dollar actively chips away at your true principal balance, letting you put your student debt behind you far sooner than the 30-year RAP horizon.

Your Next Crucial Steps

The absolute worst strategy you can deploy right now is avoidance. With servicers transitioning millions of accounts simultaneously, processing backlogs are highly likely, and administrative errors can happen.

Log directly into the official StudentAid.gov portal this week. Download your complete master promissory notes, archive your current payment histories, and use the official digital calculators to simulate your exact monthly obligations under these new federal guidelines. Taking an hour to audit your timeline today can shield you from an unexpected financial shock next month.

You may be interested in Financial Aid for US Online Students.